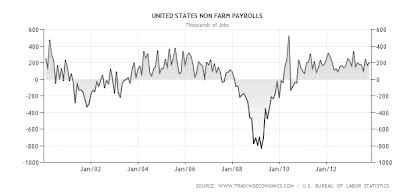

This week's housing numbers from the US should help the Fed move on at the appropriate time from QE-infinity. The S&P/Case-Shiller Home Price index showed a move up by 13.3% from a year earlier. Building permits in U.S. were up 6.2% in October to five-year high.

Housing, along with employment is central to the Fed starting to taper. Investors need to keep an eye on Case Schiller as it's my belief any weakness will be jumped on by the uber-doves at the Fed to backslide.

Both of these indices remain at multi year lows due to the fact that the Fed and ECB basically limit their ability to move higher for extended periods by effectively selling a free put to the market via QE. Thus every time the markets try to move down a wall of money dampens the effect. If you believe that QE in the US gets scaled or tapered in (say) March one could expect the breadth of the markets moves to increase and with it volatility.

This blog likes to go back to basics when inflexion points, such as a Fed taper seem to be getting closer. Below is a chart of the S&P500 v. the Put/Call ratio on the CBOE. The thing to note is that although there was a blip up last week in the ratio indicating that there were investors in the market looking to buy protection for their portfolios. The converse is that said ratio remains reasonably low and indicates to me investors are almost "sleep-walking" their way to record highs. This of course spells danger; if not for the implicit "Bernanke Put" an move downward would be magnified. Investors should keep a close watch on this ratio, noting that the lower the ratio moves indicates the greater the complacency in the market in respect to the current market levels.

A friend called me earlier today to say he was looking at a retailing opportunity in the bicycle space. He's a pretty dry character when it comes to due diligence and therefore is far better qualified to look at the sector then someone like me who's passionate about the sport. I gave him my general views about shops and retailers I've dealt with. Both of us agreed that in terms of time v. cost there's something missing in the bike servicing area. As I said recently I've never felt like I've been over-charged by a bike shop for a service. It seems ludicrous to me that somewhere between $80 - 100 gets you a good service that usually gets you on the road without any problems, which I consider to be a bargain now days. Add to this the fact there's a shortage of bike mechanics and you wonder why the price point isn't under more upward pressure. It all reminds me of the growth in high end watches and the restricting factor that is the lack of watch makers. As an example Rolex actually started an academy system in the US where they helped graduates setup shops. They literally trained you and wrote you a cheque knowing that if they couldn't meet the servicing demand consumers would drift away to cheaper more easily maintained time pieces. Perhaps we'll see the major manufacturers of bikes do the same thing? Think about it this way; you hand over your $3000 for a mid-range carbon frames bike. The experience is great until you hear a click in the bottom bracket or have a derailleur that gets out tune. If the mechanic you take it to doesn't fix it you start to think this bicycling thing is nuts . . . the result is one expensive dust catcher in the garage.

My Cannondale has been making some odd noises. The most obvious adjustment has been the headset. Readers will know that I've always had the odd issue with headsets and find the lack of science involved with adjusting them to be somewhat puzzling, especially because carbon framed bikes are quite precise in terms of the distribution of forces within the components and frame. In my case I've tightened the headset cap in the usual manner; try an eighth of a turn, ride, test and adjust again. Here's video from GCN showing how to adjust the cockpit on a carbon framed bike:

The thing to note here is the way he tightens the various bolts a little at a time so as to not focus all the forces on one small area. You see most of these type of components work to spread the load across the frame etc. Also note the use of a proper torque wrench. I've said it before, but it's worth repeating . . . buy a torque wrench and don't try and skimp on the cost. A$200 wrench will save a $4000 frame etc. You have been warned.

Ciao!